Is Your Bank Your Real Landlord?

The “Buy 1, Free 1” Mortgage Trap and How to Claim Your Title 15 Years Sooner

As a professional mortgage consultant, I see many Malaysians celebrate when their loan is approved. Whether it is a family home in Subang, a retail lot in Bukit Bintang, or industrial land in Nilai, the focus is usually on the “Monthly Installment.”

But there is a “Fourth Question” that determines your financial freedom: “How many years of my life am I working solely to pay the bank’s profit?”

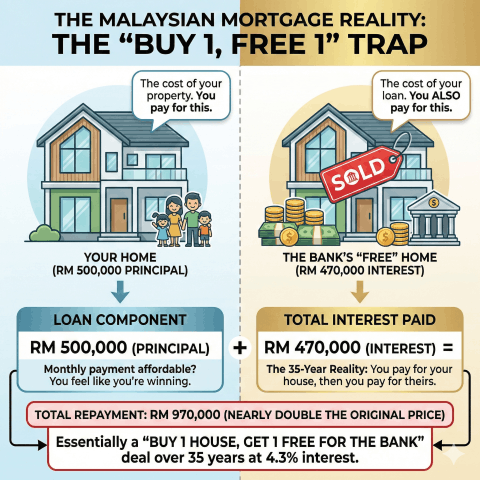

I. The “Buy 1, Free 1” Reality Check

Most homeowners believe that if they can afford the monthly payment, they are winning. Let’s look at the math for a standard RM 500,000 loan at 4.3% interest over 35 years:

| Loan Component | Total Amount | Impact |

| Loan Principal | RM 500,000 | The cost of your property. |

| Total Interest Paid | RM 470,000 | The cost of your loan. |

| Total Repayment | RM 970,000 | Nearly double the original price. |

The Reality: In Malaysia, a 35-year mortgage is essentially a “Buy 1, Free 1” deal for the bank. You pay for your house, and then you pay for theirs.

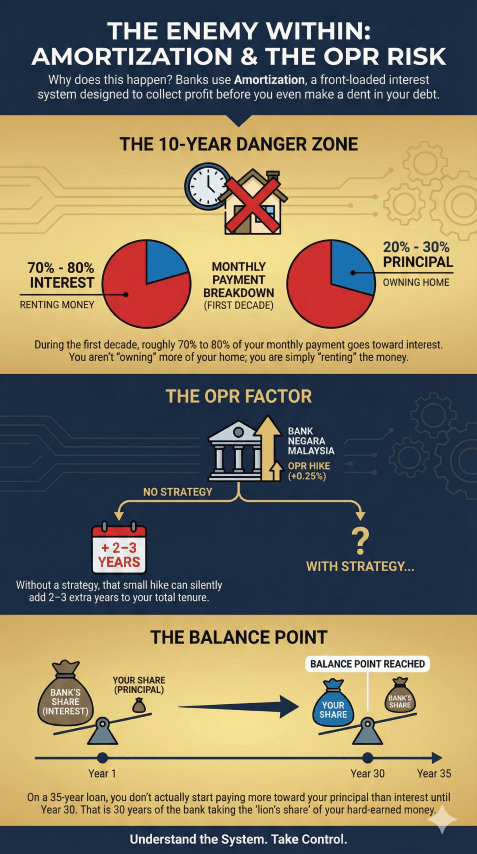

II. The Enemy Within: Amortization & The OPR Risk

Why does this happen? Banks use Amortization, a front-loaded interest system designed to collect profit before you even make a dent in your debt.

- The 10-Year Danger Zone: During the first decade, roughly 70% to 80% of your monthly payment goes toward interest. You aren’t “owning” more of your home; you are simply “renting” the money.

- The OPR Factor: When Bank Negara Malaysia raises the Overnight Policy Rate (OPR) by just 0.25%, it doesn’t just increase your monthly payment. Without a strategy, that small hike can silently add 2–3 extra years to your total tenure.

- The Balance Point: On a 35-year loan, you don’t actually start paying more toward your principal than interest until Year 30. That is 30 years of the bank taking the “lion’s share” of your hard-earned money.

III. The “Latte Factor” of Mortgage Freedom

Many believe saving RM 200,000 in interest requires a massive lump sum. It doesn’t.

The Power of Small Shifts: For the price of two premium coffees a day (approx. RM 30), a strategic extra payment of RM 900/month on a RM 500k loan can slash your interest by over RM 150,000 and shave 10 years off your tenure.

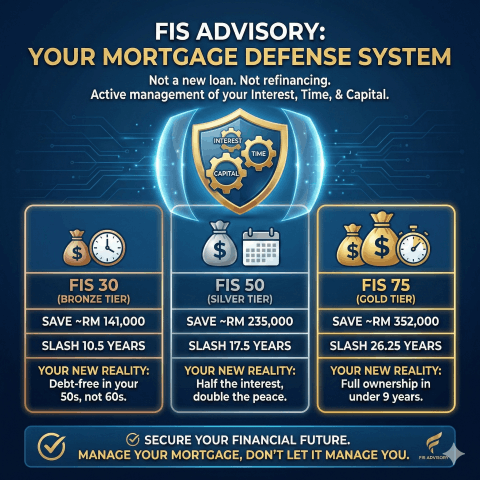

IV. The Solution: Future Interest Solution (FIS)

FIS Advisory isn’t a new loan or a refinancing trap. It is a Mortgage Defense System that manages your Interest, Time, and Capital.

| Strategy Level | Interest Saved | Years Slashed | Your New Reality |

| FIS 30 | Save ~RM 141,000 | 10.5 Years | Debt-free in your 50s, not 60s. |

| FIS 50 | Save ~RM 235,000 | 17.5 Years | Half the interest, double the peace. |

| FIS 75 | Save ~RM 352,000 | 26.25 Years | Full ownership in under 9 years. |

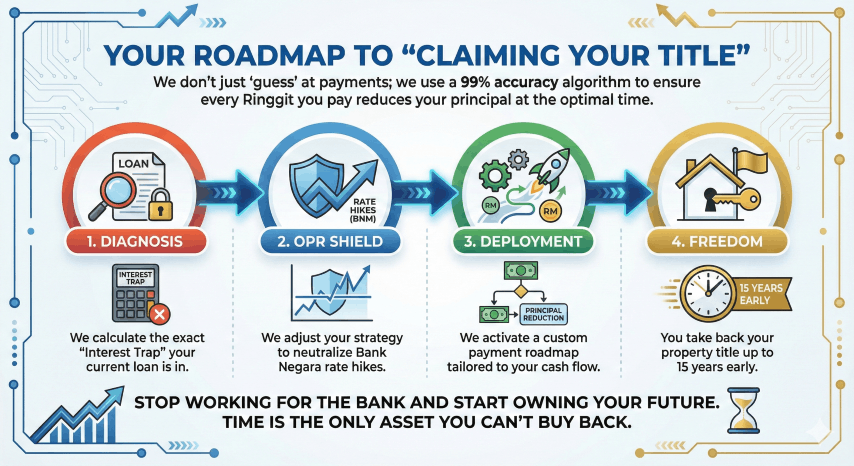

V. Your Roadmap to “Claiming Your Title”

We don’t just “guess” at payments; we use a 99% accuracy algorithm to ensure every Ringgit you pay reduces your principal at the optimal time.

- Diagnosis: We calculate the exact “Interest Trap” your current loan is in.

- OPR Shield: We adjust your strategy to neutralize Bank Negara rate hikes.

- Deployment: We activate a custom payment roadmap tailored to your cash flow.

- Freedom: You take back your property title up to 15 years early.

Stop working for the bank and start owning your future. Time is the only asset you can’t buy back.

Would you like me to prepare a checklist of the specific documents needed for your first FIS diagnostic assessment?